News

Case-Study: Testing Climate-Related Credit Risk with Real Earthquake Scenario

Background – Considering Climate-Related Credit Risk Today

As community and regional banks consider climate-related credit risks, they typically start by trying to understand the potential impact of acute climate events on the borrowers in their portfolio most vulnerable to severe events like floods, wildfires, earthquakes and drought. The specific type of acute climate related risk event will vary by the institution’s geographic footprint and location of its collateral – typically focusing on commercial and residential real estate.

Not surprisingly, typical concerns for those banks located near most U.S. coastal areas are flooding and hurricanes, while in the Southwest wildfires are a major concern. In the Midwest, tornadoes and river flooding are worries, while in the Northwest, earthquakes and mudslides are major events that can damage borrower holdings. Some areas have combinations of perils, and most lenders today do consider some degree of environmental risk when loans are made.

The US Government, through FEMA, offers a National Risk Index Score (“NRI Score”) that ranks the relative likelihood and severity of 14 specific types of acute climate-related risk events by US county and Census Tract. These events include events that involve Flooding, Strong Wind, Severe Storm, Heat and Drought, Winter and Cold and Geologic events. These ratings can help a bank identify borrowers and their collateral who are located in the highest risk areas of the country.

In mid-2023, Ardmore conducted a climate-related concentration analysis for a bank with $7+ billion in assets in Washington, with the details of that analysis presented in a Bank Director webinar on September 26th. The results of that analysis were also presented to the Bank’s management and Board, and were well received. To achieve the concentration analysis, Ardmore mapped the Bank’s collateral locations to NRI Scores at the census tract level, and produced a heat map of higher risk locations and their portfolio exposure. More information about Ardmore’s climate-related credit risk proof of concept analysis are available in this whitepaper published on June 30, 2023.

Climate-Related Credit Risk Scenario Testing

While concentration risk management is an important part of overall credit risk management, the results can be viewed by some as being only general background information and not necessarily “actionable”. A scenario test, sometimes also called a concentration stress test or sensitivity test is more targeted to a specific credit event or market condition that institution management is concerned about.

CRE credit risk management scenario testing could be prompted by a possible event such as the elevation of interest rates or a trend like the threat of the collapse of the investment office property segment. In the realm of climate-related credit risk, testing a specific acute climate event like a hurricane or an earthquake in a specific location can be very useful to identify real possible risk of repayment for a Bank.

Since the Bank which used the scenario test is located in Washington – which is known to be prone to seismic activity and the resulting destruction and linked events like landslides – earthquakes seemed to be a reasonable scenario to test.

Impact of Earthquakes and Tremor Events

As background, in March of 2014 the area of Oso, Washington was almost totally destroyed by an earthquake tremor and resulting mudslide that claimed human lives and properties in tragic proportion. While not considered a major national climate event, the landslide moved about 18 million tons of sand, till, and clay – an amount of material that would cover approximately 600 football fields each ten feet deep. Data collected shows a magnitude 1.1 earthquake on that date in the vicinity of the Oso landslide – though that small a tremor may have not been the main cause of the landslide itself. The area is historically unstable, with six other similar events of varying magnitude since 1937.

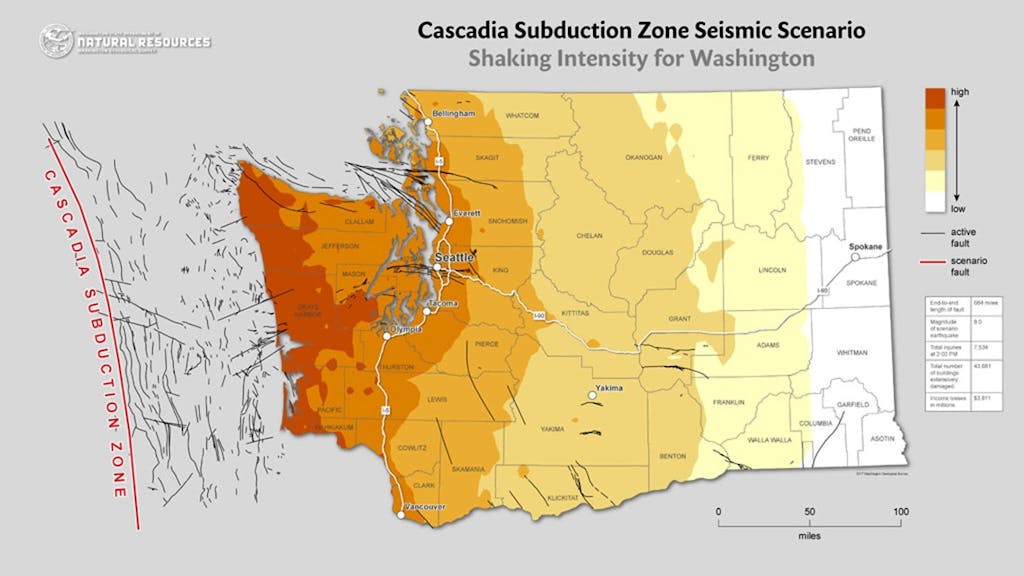

Washington has the second highest risk in the U.S. of large and damaging earthquakes because of its geologic setting. Leveraging information from Washington State Department of Natural Resources called “The Washington State Earthquake Hazards Scenario Catalog”, the Bank selected an area of about 77 square miles of nearby geological activity referred to as “Cascadia” as the area for their earthquake scenario test. Borrowers in this area represented a significant exposure of the Bank’s commercial and residential collateral – about one third of their total CRE and Residential lending book. That area also included the “Oso” location of previous seismic events.

Constructing the Scenario Test

For this scenario test, Ardmore again used the publicly available NRI scores which rank the likelihood of and severity of 14 different acute climate risk events. These scores are also categorized by FEMA into bands of severity from low to very high. By associating the location of loan collateral with a county or census tract, a bank can build out concentrations of high-risk climate-related risk severity loan concentrations.

Since the Bank had previously participated in climate-related credit risk concentration testing, their portfolio collateral locations had already been sourced from their CRA system by census tract and loaded into a credit database. To successfully perform the scenario test, a few additional steps needed to be completed by the Bank.

The Bank had identified Cascadia as the geographic sector to shock for the earthquake, so the loans with collateral in that sector would have to be flagged for analysis. The Bank had to research and provide census tract numbers for the high impact zone. Once those loans in those locations were tagged as in an “earthquake concentration” in the credit database they could be selected by a filter for the scenario test.

After the high-risk concentration loans were identified they needed to be logically pared down to those that have enough of a size and are of a type of loan that made sense to test. Criteria to consider included eliminating non-real estate related loans and loans with government guarantees. Very small size loans were also excluded as they would have minimal impact on the overall test results. Another option considered was to only select loans for the test with the highest earthquake NRI Score based on census tract – logically those that are the most vulnerable to loss.

The final piece was to gather loan financial information for testing in the financial shock scenario. Typically, the most current and accessible data point is “collateral value” as that is commonly held in bank core systems. Other helpful financial data items for expanding the testing would include annual debt service, property NOI/Cash flow and cap rates. In this case, the only financial data readily available for this scenario test was the property’s collateral or appraised value. This data was gathered and applied to the larger, highest earthquake risk-scored loans in the Cascadia earthquake zone.

There are a number of ways to apply stress/shock scenarios. In the CRE world we look at peak to trough historical valuation changes, and typically show a moderate and severe market impact. (For example, the largest known value loss percentage realized in the great recession for a particular CRE property type in the bank’s market would be a “severe” shock while half of that amount might be “moderate”.) Economic projections from reliable sources like Moody’s-REIS and CoStar as well as assessments from local appraisers can also be factored in the shock amounts.

Results of the Scenario Test

Under an earthquake scenario, different shocks can reflect the severity of financial impact in different ways. For example, as depicted in the map of the Cascadia seismic zone as provided by the State of Washington there are bands of severity based on distance from the center of activity. One could identify loans in census tracts that are in the most severe zone and shock them with a 100% loss and then a 75% for the next band out. Alternatively, there may be actual published loss estimates from similar acute climate events, and that can used as a benchmark. In any case, documenting the logic used to create the shock amounts in the scenario tests is important.

The Bank decided for expediency to simply only shock the loans that were rated “extremely high” in NRI earthquake rating bands within the earthquake zone, and apply a 100% loss value to those loans. While this stress testing methodology creates a valid view of potential loss of borrower collateral value from a severe earthquake event in the area, it is primarily directionally correct and could be more detailed. Additional Bank resources for financial data gathering and geographic filtering would be required to improve the specificity on this scenario test.

The first scenario test applied a shock of 100% loss to all properties with valuation data present in the earthquake zone. Technically, this isn’t a stress, since 100% loss means that the exposure value for all loans is lost – in this case that loss would reflect about $59 million in exposure – from the 35 eligible credits rated to be of the highest risk in the portfolio. To quote one of the credit managers at the Bank “it would be a tough day if we had to write all that off.”

To be even more conservative, we added in a 75% average loss stress to the rest of the commercial loans with collateral in the earthquake zone, a scenario which would create a total loss would be approximately $217 Million, or just over five percent of the Bank’s entire commercial portfolio’s exposure. That would be a very tough day for the Bank, indeed, and reflects a scenario that could very well happen. While the scenario results didn’t change the Bank’s policy, it did raise awareness of significant hidden climate-related credit risk within Bank to management and the board.

Conclusion

In 2024, the largest banks in the U.S. (and the world) are already dedicating resources to performing climate-related credit risk management including concentration identification and scenario stress testing exercises. Regulatory frameworks, pending rules from the SEC and other government agencies are ready to be applied to the largest US financial institutions now.

Smaller, regional and community-sized banks are beginning to understand how to leverage existing credit tools and processes to start to understand the magnitude of climate-related credit risk to their institutions. Time-tested risk management best practices like concentration management and scenario stress testing can be applied to this emerging area of climate-related credit risk. Acting in 2024 will inform bank management, the Board and regulators that the bank is proactively looking at this risk like any other risk the bank must manage now and in the future.

Banks that have a business footprint in areas prone to acute climate risk events, like earthquakes, hurricanes and wildfires can build simple methodologies to assess their current and future risk from such events. This process is rapidly becoming part of the fabric of credit risk management today for banks of all sizes.